China Chunlai Education (1969.HK): interim profit up 52% year-on-year, the future can continue to be strong

uSMART盈立智投 05-27 16:42

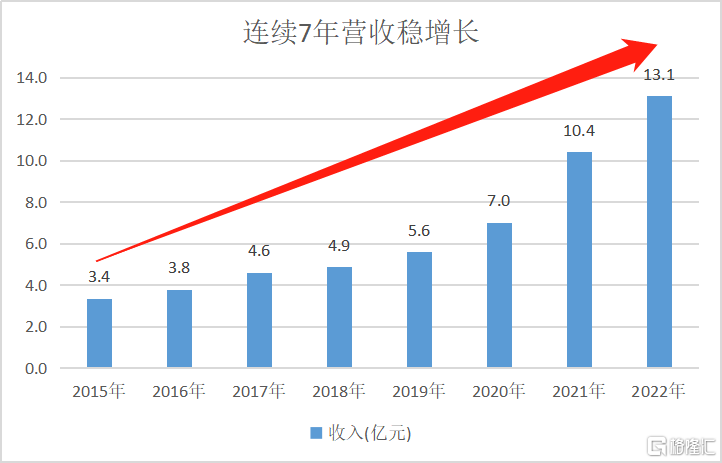

On May 26, China Chunlai (1969.HK) released its FY2022 interim report, For the six months ended 28 February 2022, the group recorded a revenue of RMB656 million, increased by 30.8% year-on-year, that means approximately RMB1.31 billion for the full year, successfully achieving 7 consecutive years of stable revenue growth.

In addition, China Chunlai realized an interim net profit of RMB251 million, up 52.4% year-on-year, and an adjusted net profit of RMB263 million, up 35.5% year-on-year. Several indicators once again confirm the robustness of China Chunlai.

The impressive performance in the first half of FY2022 is a good indication that China Chunlai's growth momentum in FY2021 continues. In FY2021, China Chunlai exceed RMB1 billion revenue, with net profit up 329.4% year-on-year and adjusted net profit up 128.7% year-on-year.

As a result of my research, multiple factors jointly drive China Chunlai's high growth in FY2021. Firstly, the enrollment size and number of students enrolled in its schools have been expanding steadily every year. More importantly, the merger of Jingzhou College after its successful transfer in May 2021 brought an additional 10,759 students to the school. The total number of students in Chunlai has exceeded the threshold of 100,000, ranking among the top 5 in the industry. In addition, China Chunlai's Anyang College Yuan Yang campus, which started enrollment in 2021, will continue to contribute to growth over the next four years.

I also note that China Chunlai has continued to rise against the trend since the new financial year, with the stock price rising by more than 60% from last year's low point, indicating that the upward channel has been opened.

Seven consecutive years of steady revenue growth

The current volatile market once again proves the famous quote from Graham, the godfather of Wall Street - "Bull market is the main reason for the loss of average investors."

As the pioneer of value investing, Graham has always emphasized the "margin of safety" and rejected Wall Street's strategy of buying fast-growing so-called "good companies" at any price. Financially sound companies, even if they do not grow at a spectacular rate, can still generate surprising returns over time through compounding.

Specifically, over the past seven years, the Group's revenue has grown at a compound annual growth rate of over 20% - a growth rate that, while not spectacular, has enabled revenue to grow several times from RMB336 million to RMB1,042 million. Behind this, China Chunlai did not overspend on future growth by going for a significant increase in tuition fees in order to create higher financial growth. The increase in enrolment has been the core driver of China Spring, with total enrolment rising from 45,210 in 2017/2018 to 107,600 in 2020/2022, a compound annual growth rate of 19%.

Since its IPO in 2018, China Chunlai's growth has further improved compared to the previous period. from FY2018-2021, the Group's revenue grew from RMB488 million to RMB1,042 million, representing a CAGR of 28.8%, while net profit attributable to the parent company grew from RMB119 million to RMB607 million, representing an even higher CAGR of 72.1%.

As you can see, net profit attributable to the parent far outpaced revenue growth, thanks to the continued improvement in profitability levels. In fiscal 2019-2021, the Group's gross margin improved by 8.1 percentage points from a high of 52.5% to 60.6%, net margin increased significantly from 24.4% to 58.3%. In the interim results, we also saw an improvement in working capital. 2022 interim results saw a 3.3% reduction in operating expenses as a percentage of revenue at 15.6%, resulting in an improvement in net margin from 32.93% to 38.26%.

I believe that with the continuous growth of revenue scale, the scale effect will gradually appear, superimposed on the Group's insistence on refined management strategy, the future period expense ratio will enter a long-term downward trend, thus promoting the company's profitability level.

In addition, the financial structure, an issue of concern to the market, continued to improve. As of the first half of 2022, the debt-to-capital ratio decreased by 23.8% year-on-year, achieving a fifth consecutive year of decline.

Intrinsic value in a headwind

In the public roadshow of China Chunlai, the management of the Group pointed out that the market will eventually return to rationality. Quality bidders like the Group, with seven consecutive years of steady revenue growth, will gradually be noticed and recognized by the market.

This has also proved to be the case. As the bubble gradually bursts, the resilience of low-priced, high-quality companies become apparent.

In China Chunlai, we see similar characteristics to those of a "public utility".

First, Low valuation. China Chunlai's current PE(TTM) is only 2.93 and P/B ratio is only 0.86, far below the average valuation level of the higher education industry.

Secondly, the "franchise" of public utilities constitutes a very high barrier to entry into the sector. Private higher education is a licensed, non-competitive market with very high barriers to entry, and a range of approvals, licenses and permits must be obtained to establish private higher education.

Third, public utilities are non-cyclical, while higher education is showing a counter trend growth. Higher education is in immediate demand, with elevated market demand for higher education in a period of intense competition for jobs. In addition, the certainty of a student's academic career is very high for three to four years after enrolment, so business does not generally fluctuate significantly.

Fourth, the higher education sector is also a cash cow business like the utilities. The way in which tuition fees are collected in advance and then spent makes the higher education sector virtually immune to working capital pressures.

From a longer investment cycle, the Group's steady growth trend is clear going forward based on the Group's dominant position. China Chunlai has a solid leading position. As at 28 February 2022, the Group owned 4 undergraduate colleges, 1 specialist college and participated in the operation of 1 independent college, with the number of students enrolled in the operating schools exceeding 100,000, placing it among the top 5 in the industry.

In addition, several favorable factors further strengthen the Group's expectations for steady growth. In addition to the measures mentioned earlier, Suzhou Tianping College is in the process of seeking a transfer in full swing. New campus completion, M&A and conversion steadily progressing, the next two to three years will be a time when many favorable factors will be released, which is expected to significantly increase the Group's profit.

China Chunlai led the rise in the higher education sector, indicating that the investors are strongly bullish on the company. At present, the policy wind is getting stronger, China Chunlai share price has support, with sufficient safety cushion, long-term imagination space is larger. Therefore, I believe that its market performance is worth looking forward to.

相關股票

中國春來(1969.HK):厚積薄發,中期利潤同比上漲52%,後市延續強勢可期

格隆匯 05-26 17:19

聯絡我們

客服專線︰+852 3018 4526

郵箱︰cs@usmarthk.com

地址︰香港上環德輔道中308號26樓2606室

WhatsApp︰+852 5989 2641